Risk Scorecards Augmented with Unstructured Data for US Lending

Hybrid AI mode

Summary

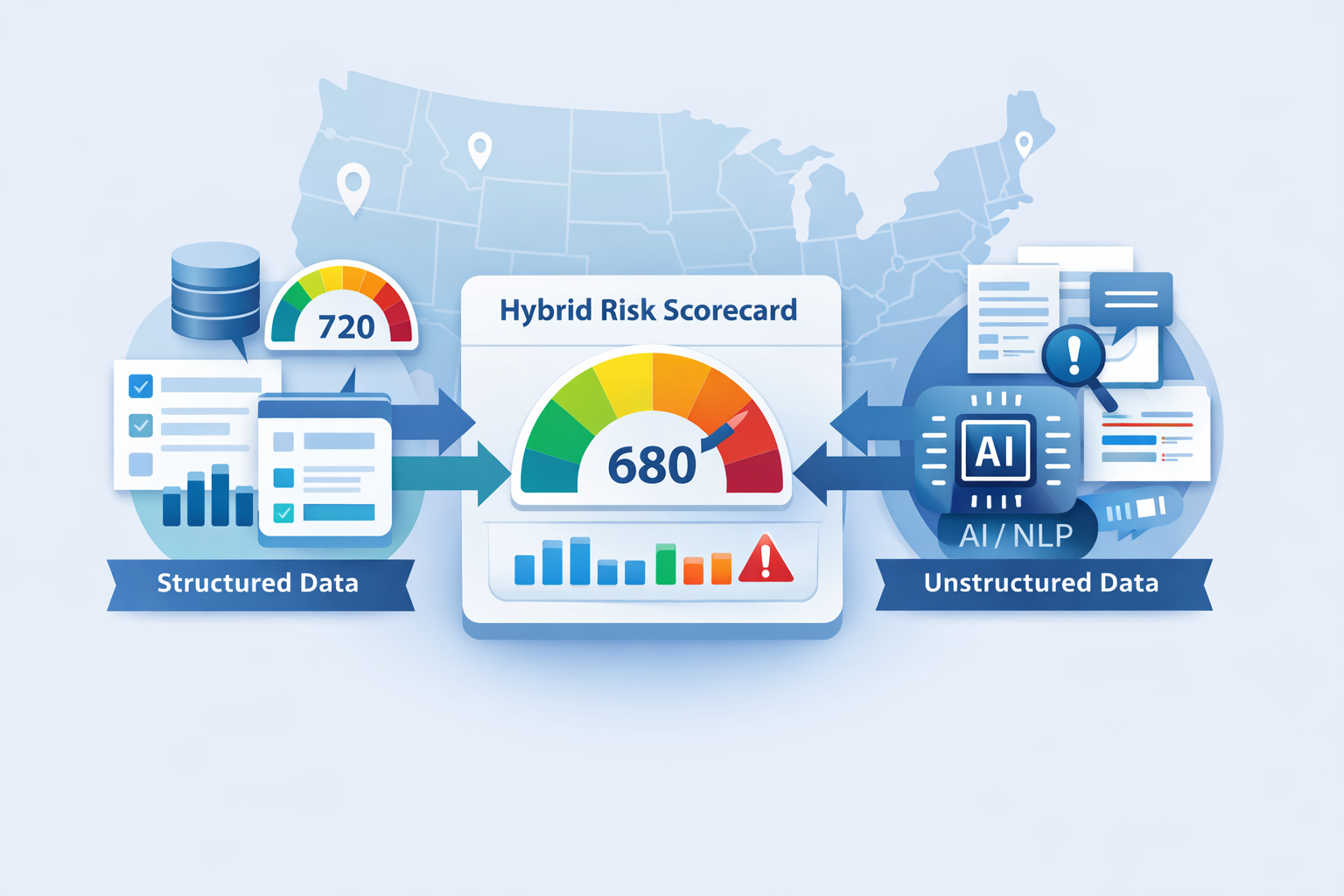

We built risk scorecards and analytical pipelines for a US payday lender operating across multiple states, serving both consumer and small-business lending. We delivered traditional scorecards (bureau data, application fields, behavioral signals) and robust ETL so operations could rely on a single, consistent risk view. On that same engagement type we also deliver an AI layer that uses unstructured data—application free text, underwriter notes, document content—to refine the score or flag edge cases that structured data alone misses.

Domain: Financial Services Operations · Lending · Risk & Compliance

Process type: Scorecard development + analytical ETL + AI augmentation on unstructured data

The Client Situation

A payday lender needed reliable risk scorecards for both consumer and small-business lending across multiple US states. The business ran on structured data: bureau scores, application fields, repayment history. Building and maintaining scorecards in a consistent way—plus ETL that fed clean, state-aware data into underwriting and operations—was the core ask. The limitation: a lot of useful signal sat in unstructured form—reason-for-loan text, employment descriptions, notes from underwriters or call centers, text extracted from uploaded documents—and wasn’t part of the score.

What We Delivered

1. Scorecards and analytical foundation

We developed risk scorecards for consumer and small-business segments, using bureau data, application variables, and behavioral features. Scorecards were built so they could be refreshed, monitored, and productionized consistently across states and products.

2. Analytical ETL and operations support

We set up analytical ETL processes so that data from multiple sources (applications, bureaus, internal systems) was cleaned, transformed, and fed into the scorecards and into lending operations. That gave the business a single source of truth for risk inputs and supported underwriting and portfolio management across multiple US states.

3. AI layer: score signals from unstructured data

We add an AI-powered layer that uses unstructured data to augment the risk view (delivered as part of this engagement type where the client needs it):

- Application free text (e.g. reason for loan, job description, income narrative): NLP/LLM extracts risk-relevant signals—consistency with structured fields, red flags, or sentiment—and feeds a secondary score or override flag that underwriting can use alongside the main scorecard.

- Underwriter or call-center notes: LLM summarization or classification helps flag inconsistencies, duplicate applications, or risk cues mentioned in notes but not in structured data, so edge cases get a second look.

- Document text (IDs, bank statements, utility bills): Extraction and consistency checks (e.g. name/address vs. application) can be automated and used as extra inputs or quality checks before the final decision.

The result is a hybrid risk model: the same proven scorecard and ETL backbone, plus optional signals derived from text and documents. The lender can keep the main decision logic in the scorecard (auditable, explainable) while using AI to surface exceptions or refine the score where unstructured data adds information.

Why Unstructured Data Belongs in the Score (When Done Right)

- Structured data (bureau, application fields, history) will always be the backbone of lending risk—regulators and ops expect it. Unstructured data (free text, notes, documents) often carries signal that never makes it into those fields: intent, consistency, or context that can improve approval accuracy or catch fraud and edge cases.

- Using AI to turn unstructured data into score inputs or flags is feasible today: LLMs and NLP can summarize, classify, and extract in a way that fits into existing scorecard and workflow design. The key is to keep the primary scorecard interpretable and use AI as an augment—not a black box replacing the whole model.

Outcome

We delivered risk scorecards and analytical ETL that gave a US payday lender a consistent, multi-state risk view for consumer and small-business lending—one source of truth for risk inputs across products and states. For clients in this setup we also deliver an AI layer on unstructured data (application text, notes, documents) so the score can incorporate signals that structured data alone doesn’t capture, while keeping the main scorecard auditable and in control. The pattern applies to any lender who wants to keep a strong scorecard backbone and add AI-powered use of unstructured data for better risk and operations.